The money arrives late. The paperwork never ends. And just when the crop cycle demands flexibility, the farm loans refuse to bend.

This is the lived reality of many farmers with farm loans in India. On paper, agricultural credit has ballooned. In reality, many farmers still grapple with credit that is mis-timed, mis-priced, and misaligned with what modern agriculture actually requires.

Institutional agricultural credit has grown dramatically over the last decade. In FY2023–24, banks disbursed over ₹20.39 lakh crore in agricultural credit, surpassing the government-set target and reflecting a more than three-fold increase over the past decade.

But despite this growth, access does not equate to adequacy. Even with rising institutional credit flows, a significant proportion of farmers, particularly small and marginal ones, still depend on informal sources like moneylenders and traders because formal credit often arrives too late or on inflexible terms. Estimates based on NSSO and other agricultural credit surveys show that informal credit remains a persistent part of rural finance, especially where formal processes are unmanageable.

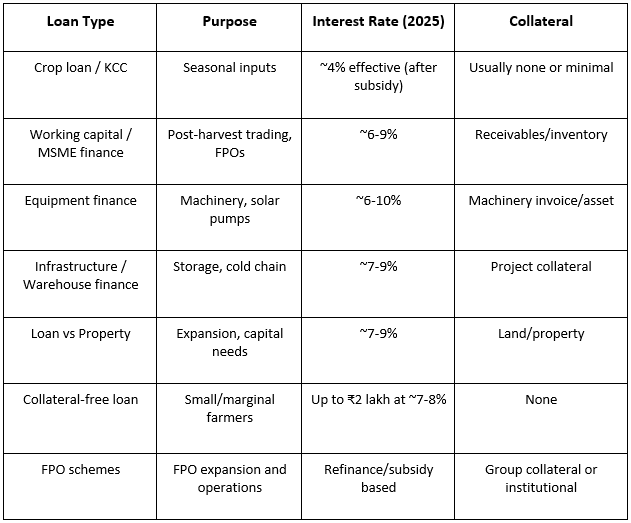

Where traditional farm loans fall short

- Timing rarely matches the crop cycle: Agriculture is time-sensitive. Production windows are short and precise, yet many farm loans are disbursed long after sowing or input purchase deadlines, undermining productivity and profitability.

- One-size-fits-all loan structures: Most farm credit products do not account for crop type, growth cycle, or market timing. Whether it’s input financing or long-term investment, conventional loans often force standardised repayment schedules that don’t align with the real cash inflows farmers experience.

- Collateral dependence limits inclusion: Formal credit often still prioritises land ownership or title, shutting out tenant farmers, sharecroppers, and others without clear collateral, despite policy efforts to widen inclusion. Reports have noted that collateral requirements remain a barrier for many smallholders.

- Credit disconnected from markets: Traditional farm loans focus on production financing. Farmers are left alone when it comes to post-harvest decisions such as storage, timing sales, and price risk management. This disconnect often leads to distress selling at harvest lows.

The cost of outdated farm loans

Post-harvest losses pose a significant economic burden on the agri-sector. While official estimates vary by crop and methodology, several agricultural studies point to post-harvest losses ranging from substantial portions of output, often cited as high as 10% for grains or much higher for perishables due to storage and supply chain gaps. Losses from premature selling or spoilage further burden the economic costs of inflexible farm loans, erasing margins before the crop even reaches the market.

What smarter farmers are choosing instead

Across India, a transformation in agricultural financing is underway. Smart farmers and agribusinesses are adopting credit models that tie funding to tangible assets, market flows, and cash cycles, not just land titles.

- Credit linked to crops and risks: Emerging agri-finance products evaluate credit risk using crop performance data, satellite insights, historical yields, and inventory positions, making financing more tailored and timely.

- Warehouse-based and post-harvest financing: With India’s warehousing ecosystem expanding under regulators such as the Warehousing Development and Regulatory Authority (WDRA), stored inventory is increasingly a bankable asset. Electronic negotiable warehouse receipts (e-NWRs) allow farmers to borrow against stored produce and sell when prices improve, reducing distress sales.

- Purpose-driven financing: Instead of blanket seasonal loans, farmers are choosing targeted credit for inputs, storage, or market timing, each structured with repayment aligned to actual economic activity, not arbitrary due dates.

- Digital, faster, transparent access: FinTech platforms leverage digital KYC, data analytics, and ecosystem integrations to reduce loan approval times from weeks to days, bringing much-needed liquidity at the right moment.

How Agriwise is enabling the smart finance shift

Agriwise is transforming agricultural credit beyond conventional farm loans. Rather than offering generic, crop-insensitive lending, Agriwise provides structured agri-financing solutions that align with how farmers actually earn and trade:

- Working capital and secured loans against property

- Inventory financing against warehouse receipts or collateral

- Credit tied to real agricultural asset value and cash cycles

- Faster digital underwriting with market and crop data integration

- Flexible repayment aligned with realised prices, not due dates

By linking credit to trade, storage, and market outcomes, Agriwise helps farmers preserve income, optimise selling timing, and reduce pressure to liquidate at low prices, moving beyond the rigid frame of traditional farm loans.

From borrowing to planning: the real shift

Smart farmers today see credit as a tool for planning, not just borrowing. Financing is integrated into decisions on when to sell, where to store, and how to time the market. This holistic approach reduces risk, improves margins, and strengthens farm economics.

Traditional farm loans still have a role, but their dominance is waning amid smarter, more integrated credit solutions. As agriculture becomes more data-driven, market-linked, and asset-oriented, credit must evolve accordingly. For farmers, the future lies not in bigger loans, but in smarter ones, built for the realities of modern farming.

FAQs

- Why do traditional farm loans fail to meet farmers’ needs?

Traditional farm loans are often rigid, slow to disburse, and poorly aligned with crop cycles, market timing, and post-harvest requirements. - How are modern farm loans different from conventional agricultural credit?

Modern farm loans are data-driven, faster, and linked to crops, storage, and trade rather than just land ownership. - What role does post-harvest financing play in improving farm incomes?

Post-harvest financing allows farmers to store produce and sell when prices are favourable, reducing distress sales and income loss. - Can farmers access credit without land ownership?

Yes, newer financing models assess crops, inventory, and trade flows, enabling access to credit even without traditional land collateral. - How does Agriwise support smarter farm financing?

Agriwise offers structured, trade-linked agri-financing that aligns credit with real cash flows, storage, and market outcomes.

Disclaimer

The content published on this blog is provided solely for informational and educational purposes and is not intended as professional or legal advice. While we strive to ensure the accuracy and reliability of the information presented, Agriwise make no representations or warranties of any kind, express or implied, about the completeness, accuracy, suitability, or availability with respect to the blog content or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. Readers are encouraged to consult qualified agricultural experts, agronomists, or relevant professionals before making any decisions based on the information provided herein. Agriwise, its authors, contributors, and affiliates shall not be held liable for any loss or damage, including without limitation, indirect or consequential loss or damage, or any loss or damage whatsoever arising from reliance on information contained in this blog. Through this blog, you may be able to link to other websites that are not under the control of Agriwise. We have no control over the nature, content, and availability of those sites and inclusion of any links does not necessarily imply a recommendation or endorsement of the views expressed within them. We reserve the right to modify, update, or remove blog content at any time without prior notice.