India’s farms are growing smarter, markets are moving faster, and finance is evolving alongside them. Today, access to the right credit at the right time can shape everything, from crop decisions to trading opportunities and long-term expansion. As institutional lending continues to expand, loans in India are becoming more digital, structured, and aligned with real agricultural needs. The country’s agricultural credit flow is projected to cross ₹32.5 lakh crore in FY2025-26, signalling both strong policy momentum and rising demand for formal financing.

But while the numbers look promising, the ground reality often tells a different story. Many farmers and agri-entrepreneurs still find themselves navigating paperwork, approval delays, and confusing loan options. The gap isn’t always about availability; it’s often about awareness and approach. Whether you’re cultivating crops, trading commodities, or scaling an agri-business, knowing how to navigate the credit landscape can make all the difference.

Here are six practical tips to help you secure hassle-free agri loans in India and make financing work in your favour.

- Maintain clear financial and land records

One of the most important steps for smooth loan approvals is proper documentation. Lenders evaluate land ownership, crop patterns, and repayment history before approving loans in India.

Keep the following ready:

-

- Updated land records or lease agreements

- Bank statements and transaction history

- Crop or business income proof

- KYC documents

- Build a strong credit profile

A strong credit history increases your chances of faster approvals and better interest rates. Over the past decade, institutional agri-credit has grown at an average of over 13% annually, showing that lenders are increasingly relying on formal credit data.

To strengthen your profile:

-

- Repay existing loans on time

- Avoid excessive borrowing

- Maintain regular bank transactions

- Use formal channels like the Kisan Credit Card or warehouse-based finance

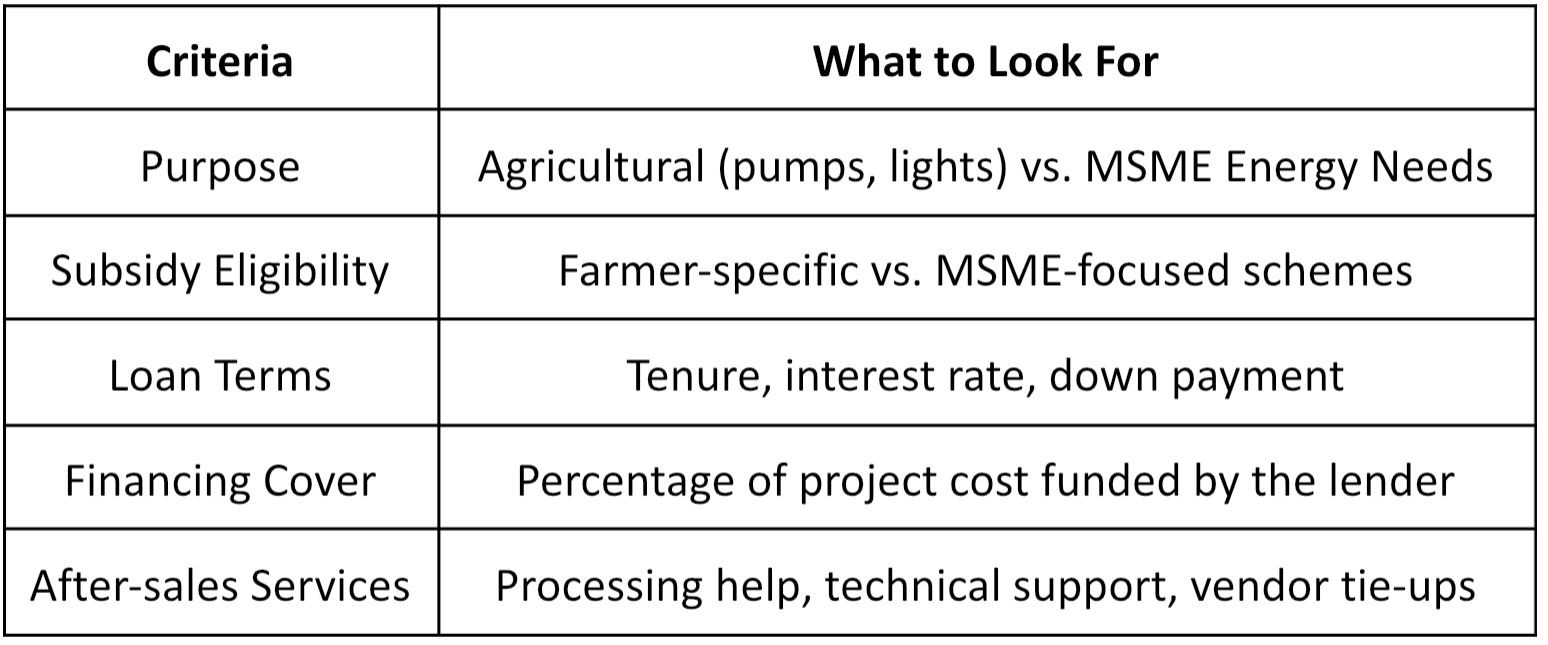

- Choose the right type of agri loan

Selecting the right financing product is crucial. Different needs require different types of loans, crop finance, equipment loans, working capital, or post-harvest funding. Applying for the wrong type of loan often leads to delays or rejection. Understanding whether you need short-term crop finance, warehouse-based funding, or long-term expansion capital can help you apply more efficiently and avoid unnecessary processing time

- Leverage digital lending platforms

Technology is transforming agri-finance. Many states now offer digital loan processing through e-Kisan Credit Card and similar systems, significantly reducing approval timelines. Recent initiatives show farmers can receive loan approvals within minutes through digital verification processes. (The Times of India)

Digital lending platforms reduce:

-

- Physical paperwork

- Branch visits

- Processing delays

- Use collateral and value-chain financing

Providing collateral or linking loans to agricultural value chains improves approval chances. For example:

-

- Stored crops can be used for warehouse financing

- Equipment or property can support secured loans

- Trade invoices can unlock working capital

With nearly 60% of agricultural lending still going toward short-term crop loans, there is a growing focus on investment and value-chain credit.

- Work with specialised agri-finance institutions

While banks remain the backbone of rural lending, specialised NBFCs and agri-finance platforms are bridging the credit gap. Even though agricultural credit targets are rising, the sector still receives a smaller share of total bank lending than mandated, highlighting the need for focused lenders.

Choosing an agri-focused lender like Agriwise offers benefits such as:

-

- Faster processing

- Sector-specific underwriting

- Flexible repayment aligned with crop cycles

- Financing for allied activities like dairy, solar, and trading

How Agriwise supports hassle-free agri financing

For borrowers seeking simplified, sector-focused credit solutions, specialised platforms like Agriwise offer financing tailored to agricultural and agribusiness needs.

Agriwise offers:

- Farmer Finance: Short-term loans for crop inputs and cultivation cycles

- Warehouse Receipt Finance: Funding against stored produce to avoid distress sales

- Loans Against Property (LAP): Secured financing for business expansion or working capital

- Solar Finance: Loans for solar pumps and renewable energy investments

Conclusion

India’s agri-credit ecosystem is expanding rapidly. Government targets, digital platforms, and value-chain financing are making loans in India more accessible than ever before. With rising institutional lending and policy support, the focus is now shifting from just loan availability to ease, speed, and suitability.

For farmers and agri-businesses, the key lies in being prepared, choosing the right lender, and leveraging digital tools. Platforms like Agriwise are playing a crucial role by offering customised solutions, from farmer finance to warehouse receipt loans, designed specifically for agricultural needs. Through these tips and working with specialised lenders, borrowers can access hassle-free agri loans and invest confidently in growth, productivity, and long-term resilience.

FAQs

- Who can apply for agri loans in India?

Farmers, FPOs, agri-traders, processors, and agri-business owners can apply for agri loans in India. Eligibility usually depends on land records or business proof, income details, repayment capacity, and basic KYC documentation. - What documents are typically required for agri loans?

Most lenders ask for identity and address proof, land ownership or lease records, bank statements, income details, and crop or business information. For value-chain financing, documents such as warehouse receipts or invoices may also be required. - How long does it take to get an agri loan approved?

Approval timelines vary by lender and loan type. Digital applications and structured financing options can significantly reduce processing time, sometimes enabling faster approvals compared to traditional methods. - What types of agri loans are available in India?

Common options include crop loans, working capital loans, warehouse receipt finance, loans against property, equipment financing, and solar or infrastructure loans. Choosing the right type based on your requirement can make the process smoother. - How can specialised agri-finance platforms like Agriwise help?

Sector-focused lenders such as Agriwise offer tailored solutions aligned with agricultural cash flows and commodity cycles. They provide financing for farmers and agribusinesses through products such as farmer finance, warehouse receipt finance, invoice discounting, and secured loans, helping make loans in India more structured and accessible.

Disclaimer

The content published on this blog is provided solely for informational and educational purposes and is not intended as professional or legal advice. While we strive to ensure the accuracy and reliability of the information presented, Agriwise make no representations or warranties of any kind, express or implied, about the completeness, accuracy, suitability, or availability with respect to the blog content or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. Readers are encouraged to consult qualified agricultural experts, agronomists, or relevant professionals before making any decisions based on the information provided herein. Agriwise, its authors, contributors, and affiliates shall not be held liable for any loss or damage, including without limitation, indirect or consequential loss or damage, or any loss or damage whatsoever arising from reliance on information contained in this blog. Through this blog, you may be able to link to other websites that are not under the control of Agriwise. We have no control over the nature, content, and availability of those sites and inclusion of any links does not necessarily imply a recommendation or endorsement of the views expressed within them. We reserve the right to modify, update, or remove blog content at any time without prior notice.