In agriculture, uncertainty is the only certainty.

From unpredictable weather patterns to fluctuating input costs and volatile commodity prices, farmers worldwide face financial pressures every season. In India, particularly, farmers are witnessing input costs rising faster than their income, a trend that puts profit margins under significant strain. Effective financial planning can make the difference between thriving and merely surviving when costs spike.

Let’s understand why and what farmers can do to plan their finances better!

Why financial planning matters in modern agriculture

Rising input costs, including seeds, fertilisers, pesticides, labour, and fuel, are among the top concerns for farmers globally. In a 2024 McKinsey farmer survey, about 48% of farmers cited increased input prices as the leading risk to profitability over the next two years, with volatility in commodity prices also gaining prominence. Overall perceived increases in costs averaged around 13%.

In India, agricultural income growth has lagged behind rural inflation, leaving farmers facing the double challenge of higher costs without commensurate income growth. Data from the Commission for Agricultural Costs and Prices (CACP) shows that while profits have risen in nominal terms, profit margins as a percentage of costs have fallen. This economic squeeze makes financial planning indispensable, not optional.

Step‑by‑step guide to financial planning for farmers

- Start with a detailed budget: The foundation of any sound financial planning is a comprehensive budget. Break your farm’s expenses into categories: fixed costs (lease, insurance, loan EMIs), variable costs (inputs like seeds and fertilisers), and seasonal expenses (labour during peak sowing or harvesting). Tools like Excel or simple farm management apps can help track and compare planned versus actual expenses regularly. Mapping out your costs allows you to identify areas where spending can be tightened and prepares you for seasonal price spikes.

- Build cash flow forecasts: A cash flow forecast estimates your expected income and expenses throughout the farming cycle. Seasonal cash flow patterns help anticipate months when funds might be tight. Use past mandi rates, contracts, and crop yield data to realistically estimate revenues. Having this roadmap lets you identify shortfalls early and arrange financing, such as formal credit or dealer financing.

- Diversify revenue sources: Don’t depend on a single crop or income stream. Diversification can be a powerful tool in your financial planning strategy. Many farmers are exploring allied activities such as livestock, high‑value horticulture, agritourism, or value‑added products to spread risk and improve resilience against volatile crop prices.

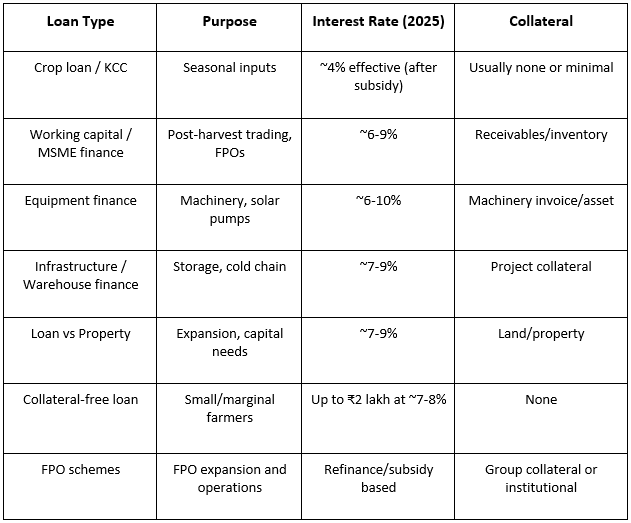

- Leverage insurance and credit products: Insurance products, such as crop insurance, help mitigate losses from weather shocks, while structured credit instruments, such as Kisan Credit Cards (KCC), provide short‑term working capital. A well‑planned credit strategy ensures liquidity during peak expenses without compromising profitability. Prioritise locking in favourable terms early and maintain good credit practices to lower interest burdens.

- Plan for emergencies: Agriculture is vulnerable to risks beyond your control, such as cyclones, unseasonal rainfall, pest outbreaks, or labour shortages. It’s prudent to set aside an emergency fund equal to 5–10% of your annual budget. Including this buffer in your financial planning not only protects you during crises but also reduces the need for high‑cost borrowing.

- Review and adjust regularly: Markets change, and so should your financial plans. Review your financial plan at least quarterly, or more frequently if input prices swing dramatically, and adjust your strategies accordingly. Timely monitoring helps you refine your projections and implement corrective actions before small issues become big problems.

The role of data and technology

Forward‑looking farmers are increasingly using technology to inform financial planning decisions. Real‑time data on weather, soil health, input prices, and market demand helps reduce guesswork and refine cost estimates. Digital tools can also automate budget tracking and alerts when expenditures exceed planned thresholds. Investment in tech might seem costly initially, but the long‑term benefits in cost control and productivity can be substantial.

Agriwise: Supporting farmers with smarter financial solutions

At Agriwise, we understand that robust financial planning is substantial for a sustainable farming business. To help farmers prepare for cost spikes and manage cash flows efficiently, Agriwise offers specialised financial solutions:

- Loans Against Property (LAP): Unlock funds by leveraging owned assets to meet financial needs.

- Warehouse Receipt Finance: Use stored agri produce as collateral to access working capital.

- Farmer Finance: Flexible credit tailored to crop cycles and seasonal requirements.

- Solar Finance: Support investments in renewable energy for farms to reduce operational costs.

Conclusion

Cost volatility is an inevitable part of agriculture, but financial hardship doesn’t have to be. Successful financial planning empowers farmers to anticipate challenges, optimise spending, diversify income streams, and build resilience against market and environmental risks. With clear budgets, smart use of credit and insurance, and regular plan reviews, farmers can not only survive cost spikes but also thrive amidst them.

By partnering with Agriwise and embracing proactive financial management, farmers unlock greater control over their economic destinies, turning risk into measured opportunity.

FAQs

- What is financial planning for farmers, and why is it important?

Financial planning for farmers involves budgeting, forecasting cash flows, and managing credit and expenses to ensure profitability despite cost fluctuations. It helps farmers anticipate cost spikes, optimise spending, and maintain sustainable operations. - How can farmers prepare for rising input costs, such as seeds, fertilisers, and labour?

Farmers can prepare by creating a detailed budget, maintaining an emergency fund, diversifying income sources, and leveraging credit or financing options to manage peak costs effectively. - What role does technology play in financial planning for farmers?

Technology provides real-time data on weather, soil health, input prices, and market trends, helping farmers make informed decisions, track expenses, and proactively adjust financial plans. - How can Agriwise services help farmers with financial planning?

Agriwise offers financial solutions, including Loans Against Property (LAP), Warehouse Receipt Finance, Farmer Finance, and Solar Finance, helping farmers access funds, manage cash flow, and plan for seasonal cost spikes efficiently. - How often should farmers review and update their financial plan?

Farmers should review their financial plan at least quarterly, or whenever there are significant changes in input costs, market prices, or crop conditions, to ensure timely adjustments and avoid financial stress.

Disclaimer

The content published on this blog is provided solely for informational and educational purposes and is not intended as professional or legal advice. While we strive to ensure the accuracy and reliability of the information presented, Agriwise make no representations or warranties of any kind, express or implied, about the completeness, accuracy, suitability, or availability with respect to the blog content or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. Readers are encouraged to consult qualified agricultural experts, agronomists, or relevant professionals before making any decisions based on the information provided herein. Agriwise, its authors, contributors, and affiliates shall not be held liable for any loss or damage, including without limitation, indirect or consequential loss or damage, or any loss or damage whatsoever arising from reliance on information contained in this blog. Through this blog, you may be able to link to other websites that are not under the control of Agriwise. We have no control over the nature, content, and availability of those sites and inclusion of any links does not necessarily imply a recommendation or endorsement of the views expressed within them. We reserve the right to modify, update, or remove blog content at any time without prior notice.