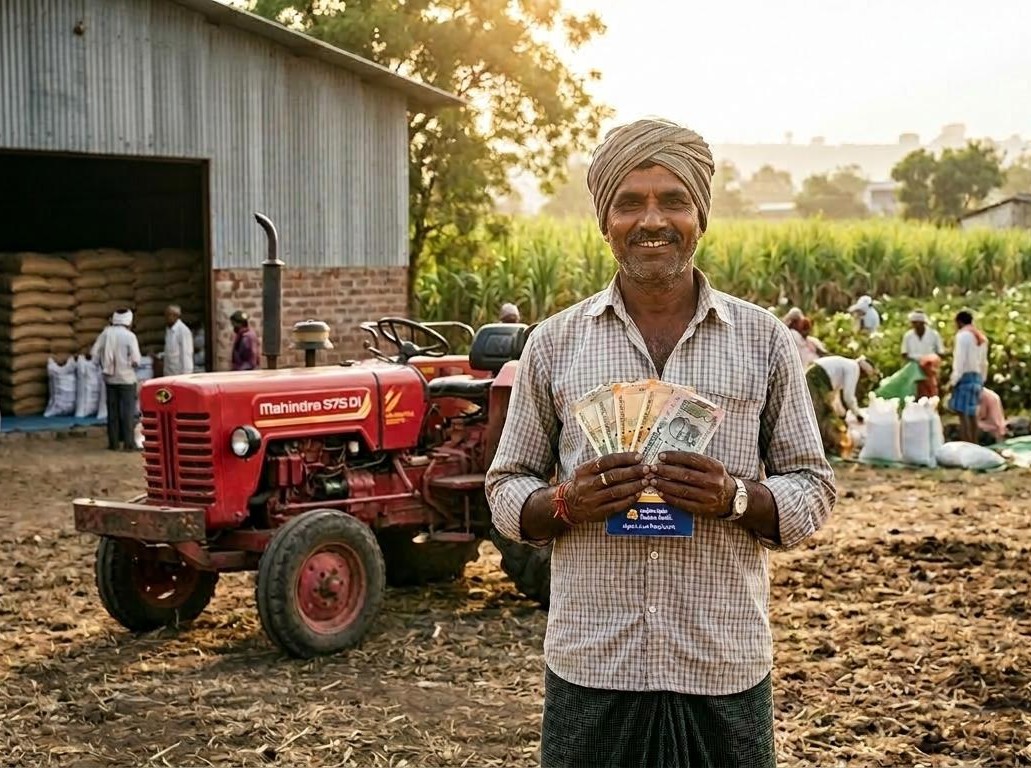

Every cropping season begins with a crucial question for millions of farmers and agri-businesses across India: how will the next crop be financed?

From purchasing seeds and fertilisers to investing in equipment and managing post-harvest expenses, agriculture requires steady access to working capital. Yet for many borrowers in rural economies, accessing timely, structured credit has historically been challenging.

In recent years, however, the landscape of agricultural lending has begun to change. With the rise of digital platforms, commodity-backed financing, and specialised agri-focused financial institutions, credit access is gradually becoming more structured, transparent, and aligned with the realities of agricultural markets. India has significantly expanded formal lending to the agricultural sector over the past decade. The Government of India set the agricultural credit target at ₹32.5 lakh crore for FY2024-25, underscoring the scale of institutional finance supporting rural and farm-based activities.

Despite this progress, many farmers and small agri-enterprises still face difficulties accessing structured credit due to limited documentation, irregular income cycles, and the inherent risks of agricultural production. This is where technology-driven financial solutions and specialised agri-finance institutions are beginning to reshape the lending ecosystem.

The credit gap in agriculture

Agriculture is a highly seasonal sector where income flows are closely tied to crop cycles. This makes traditional lending models, often designed for salaried or urban borrowers, less suited to the realities of farming.

Several structural challenges continue to limit credit access:

- Limited collateral documentation for farmers

- Difficulty in assessing crop productivity and repayment capacity

- Continued dependence on informal credit sources in rural areas

- Delays in loan approvals during critical crop seasons

According to the National Bank for Agriculture and Rural Development (NABARD), rural credit demand continues to grow as farmers increasingly invest in mechanisation, irrigation, and improved farming inputs. Improving access to structured credit is therefore essential not only for farmers but also for the broader agricultural value chain.

The rise of data-driven agri lending

Digital technologies are helping financial institutions better understand agricultural risks and borrower profiles. Using satellite data, digital land records, farm analytics, and commodity market intelligence, lenders can evaluate agricultural borrowers with far greater accuracy than before.

Data-driven lending models allow institutions to assess factors such as:

- Farm size and cropping patterns

- Historical crop productivity

- Commodity price trends

- Post-harvest storage capacity

Digital platforms are also simplifying loan processes by enabling:

- Faster loan processing and approvals

- Improved borrower verification

- Better monitoring of crop performance during the loan cycle

As a result, technology is gradually transforming agricultural lending from a high-risk segment into a more structured and data-backed financial ecosystem.

Commodity-backed financing is gaining momentum

One of the most important developments in agri-finance is the increasing adoption of commodity-backed lending models, particularly warehouse receipt financing. Under this model, farmers and traders can store commodities in certified warehouses and obtain credit against the stored produce. This allows borrowers to unlock working capital without immediately selling their crops.

This approach offers multiple benefits across the agricultural value chain.

For farmers

- Ability to avoid distress selling after harvest

- Access to immediate liquidity

- Opportunity to sell produce when market prices improve

For traders and agri-businesses

- Improved working capital management

- Better inventory planning

- Ability to leverage stored commodities for financing

Warehouse receipt financing has grown steadily as more financial institutions recognise the transparency and security offered by collateral-backed lending.

Technology is improving credit accessibility

In addition to collateral-backed lending, digital financial platforms are expanding access to credit through innovative financing models.

Some of the emerging solutions include:

- Invoice discounting for agri-businesses

- Supply chain financing

- Digital loan processing platforms

- Asset-backed lending models

By integrating financial services with supply chain data and commodity market insights, lenders can design more customised financial products for agricultural borrowers. This becomes increasingly important as India’s agricultural ecosystem becomes more commercialised and connected to national and global markets.

Agriwise’s role in strengthening agri-finance

Agriwise Finserv focuses on providing specialised financial solutions tailored to the agricultural ecosystem. By combining financial expertise with a deep understanding of agricultural supply chains, Agriwise aims to bridge the gap between credit demand and structured financing solutions.

Agriwise offers a range of financial products designed to support farmers, traders, and agri-businesses, including:

- Warehouse Receipt Finance

- Supply Chain Finance

- Loans Against Property (LAP)

- Farmer Finance

- Solar Finance

These solutions help borrowers access working capital for agricultural operations, trade activities, and rural infrastructure investments.

Agriwise leverages the broader StarAgri ecosystem, including warehousing infrastructure, commodity intelligence, and agri supply chain insights, to enable financing solutions that are aligned with the operational realities of agricultural markets.

The road ahead for agri-finance

As agriculture becomes increasingly technology-driven and market-oriented, the role of structured financial services will continue to expand.

Future developments in agri-finance are likely to focus on:

- Greater integration of digital farm data and credit assessment

- Expansion of collateral-backed lending models

- Wider adoption of supply chain financing platforms

- Increased participation of specialised NBFCs in agricultural lending

These innovations have the potential to significantly improve financial inclusion across rural India while strengthening the agricultural value chain. With data-driven insights, supply chain infrastructure, and specialised financial products, the next generation of agri-finance solutions can help create a more resilient and accessible agricultural economy.

FAQs

- Why is access to credit important for farmers and agri-businesses?

Access to timely credit helps farmers and agri-businesses manage input costs such as seeds, fertilisers, equipment, and labour. Structured financing also enables businesses in the agricultural supply chain to manage working capital and invest in productivity improvements. - What are the main challenges in agricultural lending?

Agricultural lending can be challenging due to seasonal income cycles, limited financial documentation, and uncertainties related to weather and crop productivity. These factors often make it difficult for traditional lending models to assess borrower risk accurately. - What is warehouse receipt finance, and how does it work?

Warehouse receipt finance allows farmers and traders to obtain loans against commodities stored in certified warehouses. The stored produce acts as collateral, enabling borrowers to access working capital without immediately selling their crops. - How is technology improving agri-finance in India?

Digital technologies such as satellite data, farm analytics, and digital lending platforms help financial institutions better evaluate agricultural borrowers. These tools enable faster loan approvals, improved risk assessment, and greater access to credit for rural borrowers. - What financial solutions does Agriwise Finserv provide?

Agriwise Finserv offers specialised financial products designed for the agricultural ecosystem, including warehouse receipt finance, invoice bill discounting, loans against property, farmer finance, and solar finance. These solutions help farmers, traders, and agri-businesses access working capital and expand their operations.

Disclaimer

The content published on this blog is provided solely for informational and educational purposes and is not intended as professional or legal advice. While we strive to ensure the accuracy and reliability of the information presented, Agriwise make no representations or warranties of any kind, express or implied, about the completeness, accuracy, suitability, or availability with respect to the blog content or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. Readers are encouraged to consult qualified agricultural experts, agronomists, or relevant professionals before making any decisions based on the information provided herein. Agriwise, its authors, contributors, and affiliates shall not be held liable for any loss or damage, including without limitation, indirect or consequential loss or damage, or any loss or damage whatsoever arising from reliance on information contained in this blog. Through this blog, you may be able to link to other websites that are not under the control of Agriwise. We have no control over the nature, content, and availability of those sites and inclusion of any links does not necessarily imply a recommendation or endorsement of the views expressed within them. We reserve the right to modify, update, or remove blog content at any time without prior notice.