As India marches toward becoming a $5 trillion economy, MSME finance and agribusiness continue to drive inclusive and sustainable growth. With nearly 63 million micro, small and medium enterprises (MSMEs) contributing around 30% to India’s GDP, and agriculture employing over 50% of the workforce, both sectors demand innovative, tech-led financial solutions.

Agricultural credit in India is projected to exceed ₹31.5 lakh crore in FY26, driven by increased formalisation of rural credit—signalling a shift toward more structured, data-backed, and accessible financial systems.

Let’s explore the key agribusiness trends and the evolving landscape of MSME credit solutions shaping India’s economic future.

1. Rise of Digital Lending Platforms

One of the most defining developments in MSME finance is the rapid growth of digital lending. Startups and NBFCs are using alternative credit scoring methods—such as transaction data, utility payments, and GST returns—to extend loans to borrowers who were traditionally excluded from the formal financial system.

This evolution is crucial as millions of businesses lack formal credit histories. Fintech for MSMEs has emerged as a lifeline, especially post-pandemic, offering fast, collateral-free access to capital—reducing dependency on unorganised lenders and improving financial inclusion across rural India.

2. Co-Lending Models: Banks + NBFCs = Wider Reach

To bridge the significant credit gap, co-lending partnerships between banks and NBFCs have gained momentum. Banks offer a lower cost of capital, while NBFCs provide last-mile reach. This hybrid approach is enabling faster and more effective disbursement of MSME loans in 2025, particularly to underserved areas.

In fact, NBFCs have become key contributors to MSME finance in India, outperforming banks in disbursement volumes in the last fiscal year. This collaboration also fosters tailored credit offerings, better suited to the real-time needs of small businesses and agri-entrepreneurs.

3. Government-Led MSME Finance Solutions

The government’s focus on MSMEs has intensified through schemes such as the CGTMSE (Credit Guarantee Fund Trust for Micro and Small Enterprises). As of late 2024, CGTMSE had facilitated over ₹5.2 lakh crore in guarantees. The recent budget also announced the introduction of MSME credit cards, offering working capital limits of up to ₹10 lakh under automatic guarantee coverage.

These initiatives are expected to enhance the accessibility of MSME loans in 2025, especially for first-generation entrepreneurs, women-led enterprises, and rural agri-based MSMEs—boosting job creation and economic resilience.

4. Green Finance: A Sustainable Future for Agribusiness

As sustainability gains priority across industries, MSME finance is also adapting. Financial institutions are offering incentives for eco-friendly initiatives—such as solar-powered agri equipment, organic farming, and energy-efficient food processing units.

This alignment with ESG (Environmental, Social, and Governance) goals is a key future trend in agri finance, helping agribusinesses reduce carbon footprints and qualify for better financing terms. Dedicated schemes, such as RAMP and green funds, are expected to drive this transition forward in 2025 and beyond.

5. Embedded Finance and Supply Chain Digitisation

With more MSMEs and agri-enterprises going digital, embedded finance—offering financial services directly within non-financial platforms—is transforming the way loans and payments are accessed. Businesses using marketplaces, ERP systems, or mobile apps can now access MSME credit solutions without leaving their digital ecosystems.

Simultaneously, digital supply chain finance is growing, supporting vendors, distributors, and processors with faster payments, credit lines, and invoice discounting. This is a critical development for agribusinesses relying on seasonal liquidity and fluctuating input costs.

6. AI-Powered Lending & Risk Assessment

The integration of AI and analytics in credit evaluation is redefining MSME finance. By utilising satellite imagery, crop monitoring data, and transaction analytics, lenders can more accurately assess risks and process loans more efficiently. This is particularly impactful in agri-finance, where traditional underwriting methods often fall short.

This data-driven approach ensures that borrowers with viable but informal operations are not left out. It also boosts credit discipline and helps institutions maintain portfolio health while serving new-to-credit segments.

7. Supportive RBI Policies & Rate Cuts

In June 2025, the Reserve Bank of India reduced the repo rate and cash reserve ratio, aiming to boost liquidity in the banking system. These changes are expected to make MSME loans in 2025 more affordable and accessible.

With MSMEs accounting for just 16% of formal credit but over a quarter of GDP, such measures are essential to balance risk and support expansion, especially in agri-linked businesses that face seasonal cash flow cycles.

The Road to MSME Finance: Empowering India’s Growth Engines

The future of MSME finance in India is poised for greater inclusion, efficiency, and resilience. Here’s a snapshot of the key agribusiness trends and financing shifts:

- Digital lending to expand credit access and formalise small businesses

- Co-lending models for deeper credit penetration in underserved markets

- Green and ESG-aligned loans to support sustainable agribusiness growth

- Embedded finance and supply chain tools for seamless MSME funding

- AI-powered crop and enterprise finance for smarter credit risk evaluation

- Policy push and credit guarantee schemes for risk mitigation and affordability

With evolving borrower needs and a supportive policy environment, these trends will drive the next wave of growth in both agribusiness and MSMEs.

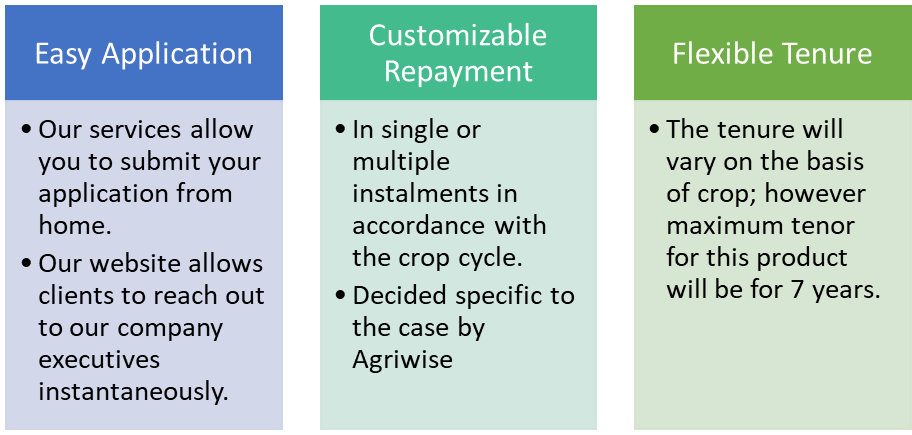

Agriwise: Enabling the Future of Agri and MSME Finance

At Agriwise, we are proud to be part of India’s evolving MSME finance journey. Our offerings are designed to empower farmers, traders, and agri-based businesses with timely, transparent, and tech-driven credit access.

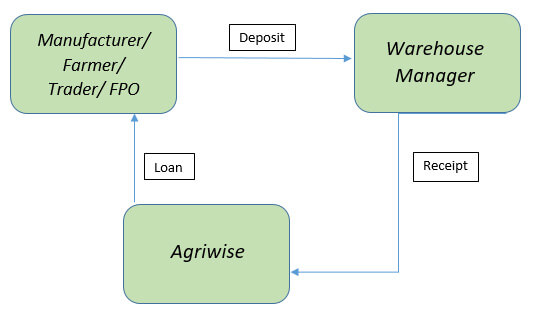

- Through our warehouse receipt financing, we help farmers turn stored produce into instant working capital, eliminating distress sales and enabling smarter price realisation.

- We combine field-level insights with data analytics and fintech tools to offer tailored credit assessments—redefining MSME credit solutions for the agri sector.

- Our growing network of bank partnerships and co-lending arrangements makes MSME loans in 2025 more accessible and flexible.

- Agriwise is also committed to sustainability, financial literacy, and empowering women and first-generation agri-entrepreneurs with responsible access to credit.

As the future of agri finance becomes smarter and more inclusive, Agriwise remains committed to enabling India’s farmers and MSMEs with the financial tools they need to succeed.