India’s MSME sector is often described as the backbone of the economy, and rightly so. With millions of enterprises, MSMEs contribute significantly to employment, exports, and industrial output.

“As of December 2025, over 7.30 crore MSMEs were registered across India through the official Udyam Registration Portal and Udyam Assist Platform, including approximately 4.37 crore registrations on Udyam and 2.92 crore on Udyam Assist. Micro-enterprises overwhelmingly dominate the sector, accounting for the vast majority of registrations.”

Yet, access to timely and adequate credit remains one of the biggest challenges for this segment. Traditional banking systems, constrained by rigid underwriting frameworks, often fail to address the evolving needs of MSMEs. This is where Non-Banking Financial Companies (NBFCs) are stepping in to redefine the lending landscape.

The MSME Credit Gap

Despite multiple government initiatives, the MSME credit gap in India remains substantial. Many enterprises, especially in semi-urban and rural areas, lack formal credit histories, making them high-risk for traditional lenders.

However, MSMEs are increasingly becoming digitally visible through GST data, transaction records, and supply chain integrations, creating new opportunities for innovative lenders.

How NBFCs Are Changing the Game

NBFCs are leveraging technology and alternative data to build more inclusive credit models that further enable MSMEs to access credit that is both timely and context-specific.

- Cash-flow-based lending instead of collateral-heavy models

- Faster disbursals through digital underwriting

- Customised financial products aligned with business cycles

- Supply chain financing for working capital optimisation

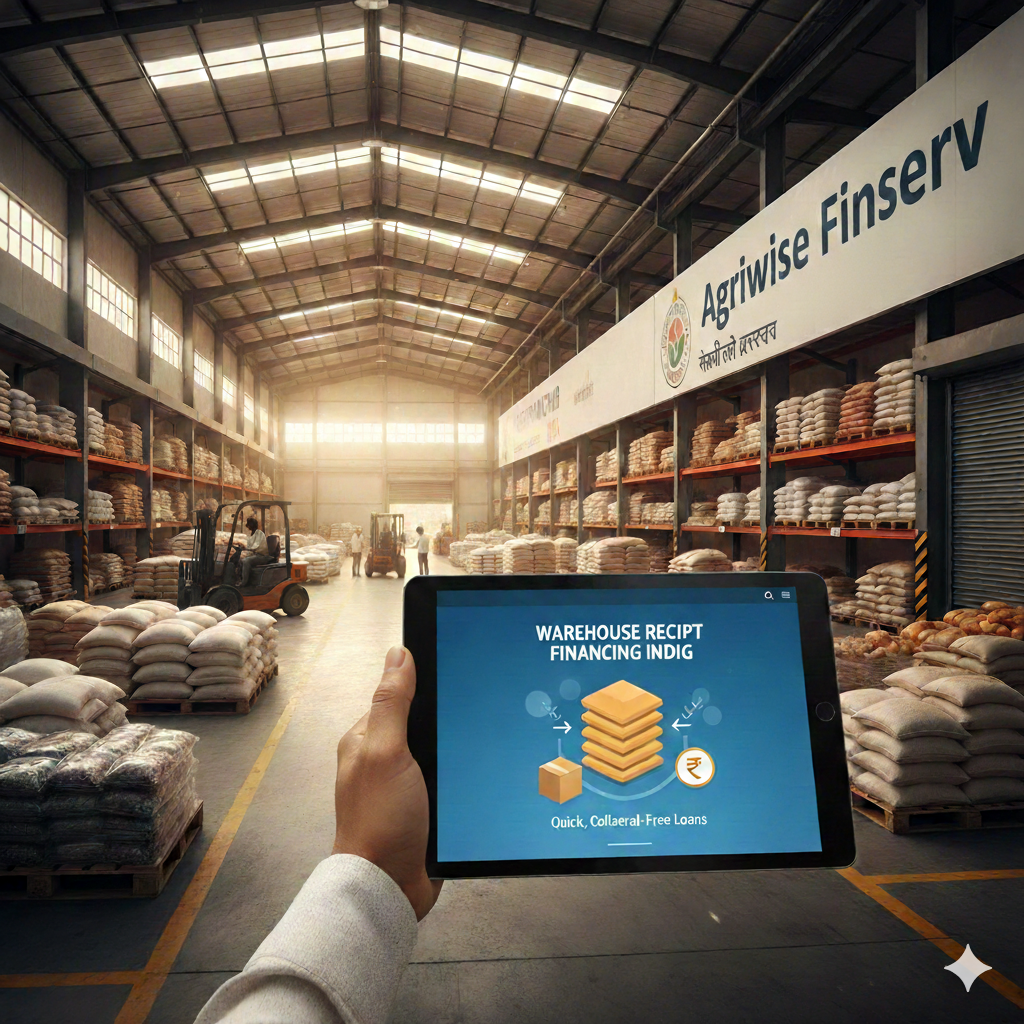

Agriwise: Bridging Finance and Agriculture

Agriwise Finserv is a prime example of how NBFCs are innovating within the agri-MSME ecosystem. Agriwise focuses on structured, asset-backed and trade-linked financing solutions, including:

- Warehouse Receipt Finance

- Invoice Bill Discounting

- Loans Against Property (LAP)

- Farmer Finance and Solar Finance

What differentiates Agriwise is its integration with the broader agri-value chain:

- Financing linked to stored commodities

- Risk mitigation through collateral management systems

- Data-driven credit decisions using platform insights

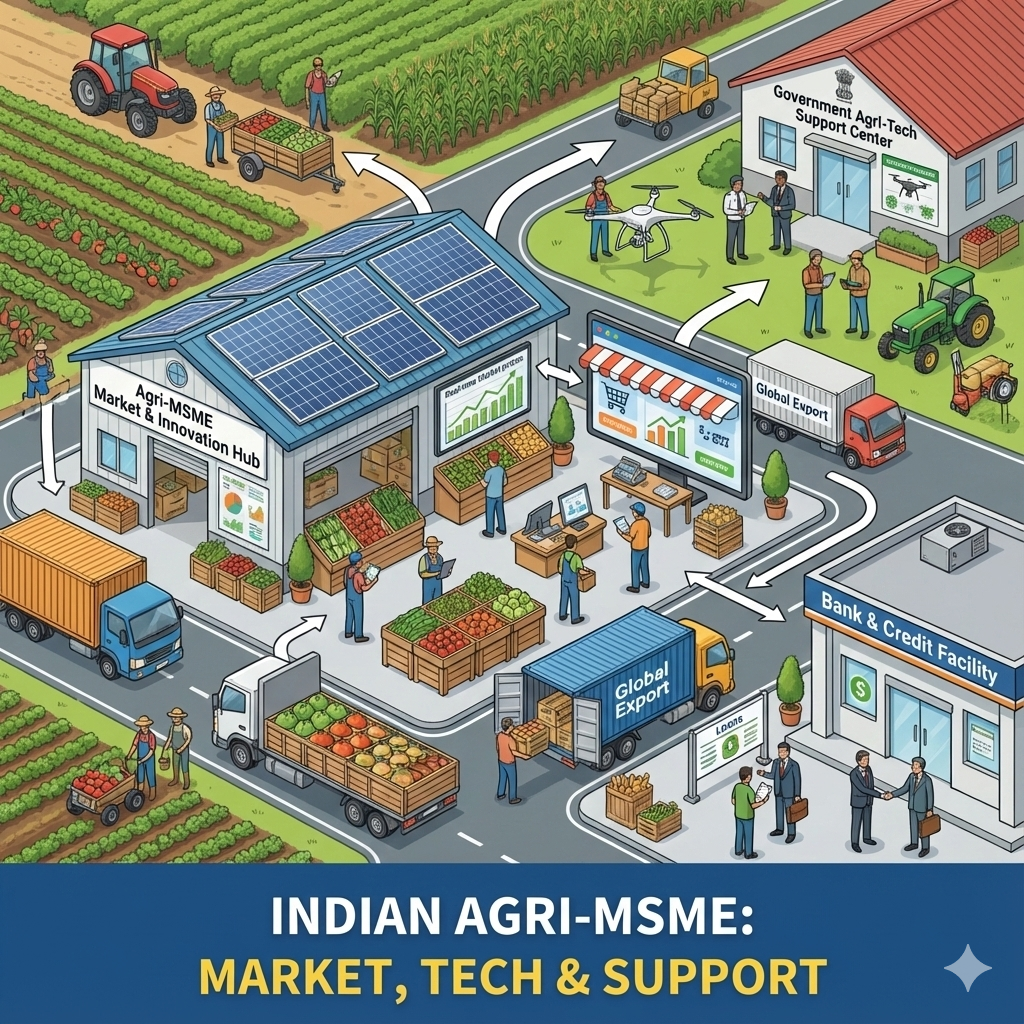

Digital Lending Meets Agri Supply Chains

The convergence of digital platforms and NBFC lending is transforming MSME finance:

- Real-time commodity prices

- Digitised warehouse records

- Satellite-based land insights (through platforms like AgriBhumi)

These innovations enable lenders to assess risk more accurately and offer better credit terms.

Government Push and Policy Support

India’s policy ecosystem is actively supporting MSME financing:

- Priority sector lending norms for agriculture and MSMEs

- Credit guarantee schemes reducing lender risk

- Infrastructure funds boosting agri-logistics

Additionally, schemes like Mudra loans provide micro-credit support up to ₹10 lakh, fostering entrepreneurship.

The Future of MSME Finance

NBFCs are reshaping the credit ecosystem. The future will likely see:

- Increased use of AI-driven credit models

- Embedded finance within supply chains

- Greater collaboration between NBFCs and fintech platforms

For agri-focused NBFCs like Agriwise, the opportunity is even larger. By aligning credit with commodity cycles, storage infrastructure, and market linkages, they can unlock significant value for MSMEs.

Conclusion

The evolution of NBFCs marks a fundamental shift. They are redefining MSME finance by shifting from collateral-based lending to data-driven, cash-flow-focused models that better reflect real business cycles. This is particularly impactful in agriculture, where seasonality and market linkages are critical.

Agriwise Finserv exemplify this change by integrating finance with the warehousing and trading ecosystems, enabling faster, more relevant access to credit. As a result, credit is increasingly becoming a strategic enabler of MSME growth rather than a constraint.

FAQs

- Why are NBFCs important for MSME financing in India?

NBFCs provide flexible, faster, and more accessible credit compared to traditional banks, especially for underserved MSMEs. - How are NBFCs changing traditional lending models?

They use cash-flow-based lending, digital data, and alternative credit assessment methods instead of relying only on collateral. - What challenges do MSMEs face in accessing credit?

Limited credit history, lack of formal documentation, and rigid banking processes often restrict access to financing. Inadequate bookkeeping, unfiled tax returns, or inconsistent cash flow records reduce lender confidence., Limited Collateral etc - How does Agriwise Finserv support MSMEs?

Agriwise offers solutions like warehouse receipt finance, invoice discounting, and integrated with agri supply chains. - What is the future of MSME financing in India?

It will be driven by digital lending, AI-based risk assessment, and embedded finance within supply chains.