As more farms turn to clean energy, solar finance has become a vital tool that helps farmers install solar pumps, rooftop systems, and field-mounted arrays without large upfront costs. This guide breaks down how solar finance works in practical steps and highlights why it’s an attractive option for small and medium farmers in India today.

Why is solar finance important for farmers?

Solar finance provides the capital support needed to transition from expensive traditional power sources to clean solar energy. India’s transition to solar is accelerating. By 2025, the country’s utility-scale and distributed solar capacity crossed the 100+ GW mark, reflecting rapid adoption across sectors. In 2025, India continued to install solar pumps, with significant progress reported under the Pradhan Mantri Kisan Urja Suraksha evam Utthaan Mahabhiyan (PM-KUSUM) scheme. As of July 31, 2025, 8.53 lakh solar pumps were installed.

These shifts make solar finance not just an environmental choice but a smart economic decision: predictable energy bills, higher irrigation reliability, and, often, access to government subsidies or favourable loan schemes.

How does solar finance work for a farmer?

- Assess energy need and costs: Estimate the system size you need (pump horsepower or kW for a roof/field system), expected energy generation, and total system cost (equipment, installation, wiring). Many local vendors or solar installers will provide a free site assessment and a quotation.

- Explore subsidies & grants: Central and state schemes frequently offer capital subsidies or incentives for agricultural solar (pump and feeder schemes, rooftop incentives). These subsidies can reduce the upfront cost and improve loan viability. Verify current schemes at the local nodal agency or state renewable energy department.

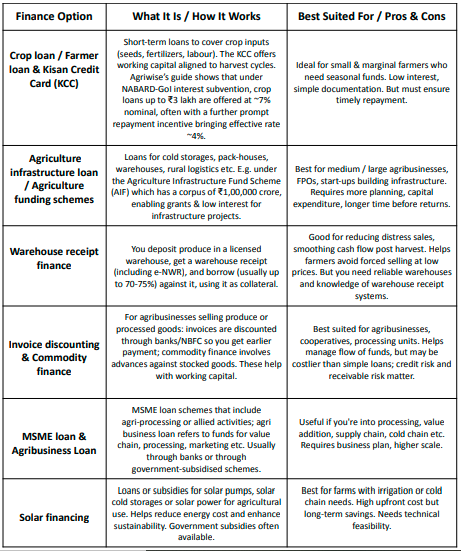

- Choose a financing option: Solar finance for farmers typically comes in several forms: Farmers have multiple avenues to finance solar installations. Government programmes such as the PM-KUSUM scheme provide capital subsidies and facilitated credit support to lower the cost burden of adoption. In addition to these subsidised mechanisms, farmers may also access conventional bank financing, asset-specific equipment loans, or secured term loans offered by banks and NBFCs.

-

- Retail/consumer loans from banks and NBFCs (secured or unsecured, with tenors matching equipment life).

- Asset-backed loans collateralised by the solar system itself.

- Pay-As-You-Go / Lease / Energy-as-a-Service models, where a provider installs and owns the system — the farmer pays a predictable monthly fee tied to energy delivered.

- Blended finance where subsidy + concessional credit + commercial loan are combined to lower the effective cost.

- Loan application and documentation: Typical documents: KYC, land proof /7/12, farm electricity bill, quotation from installer, and subsidy sanction proof (if applicable). Lenders will assess repayment capacity, often using projected savings from fuel/electricity substitution and any additional farm income generated from reliable irrigation or cold-storage power.

- Installation and inspection: After loan sanction and disbursal (sometimes partly to the vendor), the system is installed. Lenders or nodal agencies may require an inspection and performance guarantees. Modern finance models include remote monitoring to ensure generation meets promised levels.

- Repayment & performance monitoring: Repayment schedules can be matched to crop cash flows (seasonal EMIs or grace periods). In meter-based or PAYG models, payments may be linked to generated energy or a flat monthly tariff. Many systems now offer remote telemetry so lenders and farmers can monitor generation and address issues fast.

Key data to consider

- India’s large-scale and distributed solar capacity surged through 2025, making the technology widely available and competitive vs. diesel alternatives.

- The solar irrigation rollout is sizeable; reports and company disclosures show tens of thousands of pump systems added in recent fiscal periods, underscoring demand from the agriculture sector.

- Sustainable agriculture finance is increasingly channelled into climate-smart investments. Green finance reports show rising flows into agri-solar projects and related lending instruments.

How Agriwise supports farmers with solar finance?

Agriwise provides farmer-centric solar finance solutions designed for agriculture realities: flexible tenors that align with cropping cycles, options for equipment financing (pumps, panels, inverters) and tie-ups with verified installers to simplify procurement. Agriwise structures loans so that subsidy benefits and projected fuel/electricity savings are integrated into the repayment plan, reducing cash-flow stress for farmers.

Quick tips for farmers considering solar finance

- Get multiple quotes; compare warranties and expected energy yield.

- Check subsidy eligibility first; it varies by state.

- Align loan tenure with expected equipment life

- Consider monitoring systems, which reduce downtime and protect your investment.

Adopting solar through smart solar finance can lower operating costs, improve irrigation reliability, and strengthen farm resilience. With the right financing partner (like Agriwise) and careful planning, farmers can switch to clean energy with minimal strain on cash flow — turning sunlight into a dependable farm asset.

Disclaimer

The content published on this blog is provided solely for informational and educational purposes and is not intended as professional or legal advice. While we strive to ensure the accuracy and reliability of the information presented, Agriwise make no representations or warranties of any kind, express or implied, about the completeness, accuracy, suitability, or availability with respect to the blog content or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. Readers are encouraged to consult qualified agricultural experts, agronomists, or relevant professionals before making any decisions based on the information provided herein. Agriwise, its authors, contributors, and affiliates shall not be held liable for any loss or damage, including without limitation, indirect or consequential loss or damage, or any loss or damage whatsoever arising from reliance on information contained in this blog. Through this blog, you may be able to link to other websites that are not under the control of Agriwise. We have no control over the nature, content, and availability of those sites and inclusion of any links does not necessarily imply a recommendation or endorsement of the views expressed within them. We reserve the right to modify, update, or remove blog content at any time without prior notice.